Bookkeeping done wrong = IRS audit risk.

Many small businesses face penalties, interest, and compliance issues due to avoidable bookkeeping mistakes. From misclassified expenses to missing 1099 forms, these errors snowball into tax problems if left unchecked.

Here are the most common mistakes we see, and how to fix them before the IRS finds them.

Misclassified Expenses or Income

Common Mistakes:

- Mixing personal and business expenses

- Categorizing meals as entertainment

- Recording owner draws as business expenses

Why It Matters:

Improper classification leads to disallowed deductions, inflated taxable income, and audit red flags.

Invoicing & Sales Tax Tracking Errors

Common Mistakes:

- Forgetting to apply sales tax to invoices

- Mislabeling taxable vs. non-taxable services

- Inconsistent rates across jurisdictions

Risk:

Incorrect collection and remittance = sales tax audit + state penalties

Incomplete Customer & Vendor Records

Issues:

Risk:

Lack of 1099 compliance exposes you to IRS fines and delayed filings.

Missed Payroll Accruals

Mistakes:

- Not recording accrued wages

- Payroll tax liabilities not tracked

- Payroll periods mismatched with accounting periods

Result:

Under reported liabilities, incorrect financials, late deposits

Owner Distributions & Fixed Asset Confusion

Errors:

- Logging owner withdrawals as regular expenses

- Expensing capital assets instead of capitalizing

Consequences:

Taxable income is understated, depreciation schedules go missing, and IRS penalties increase.

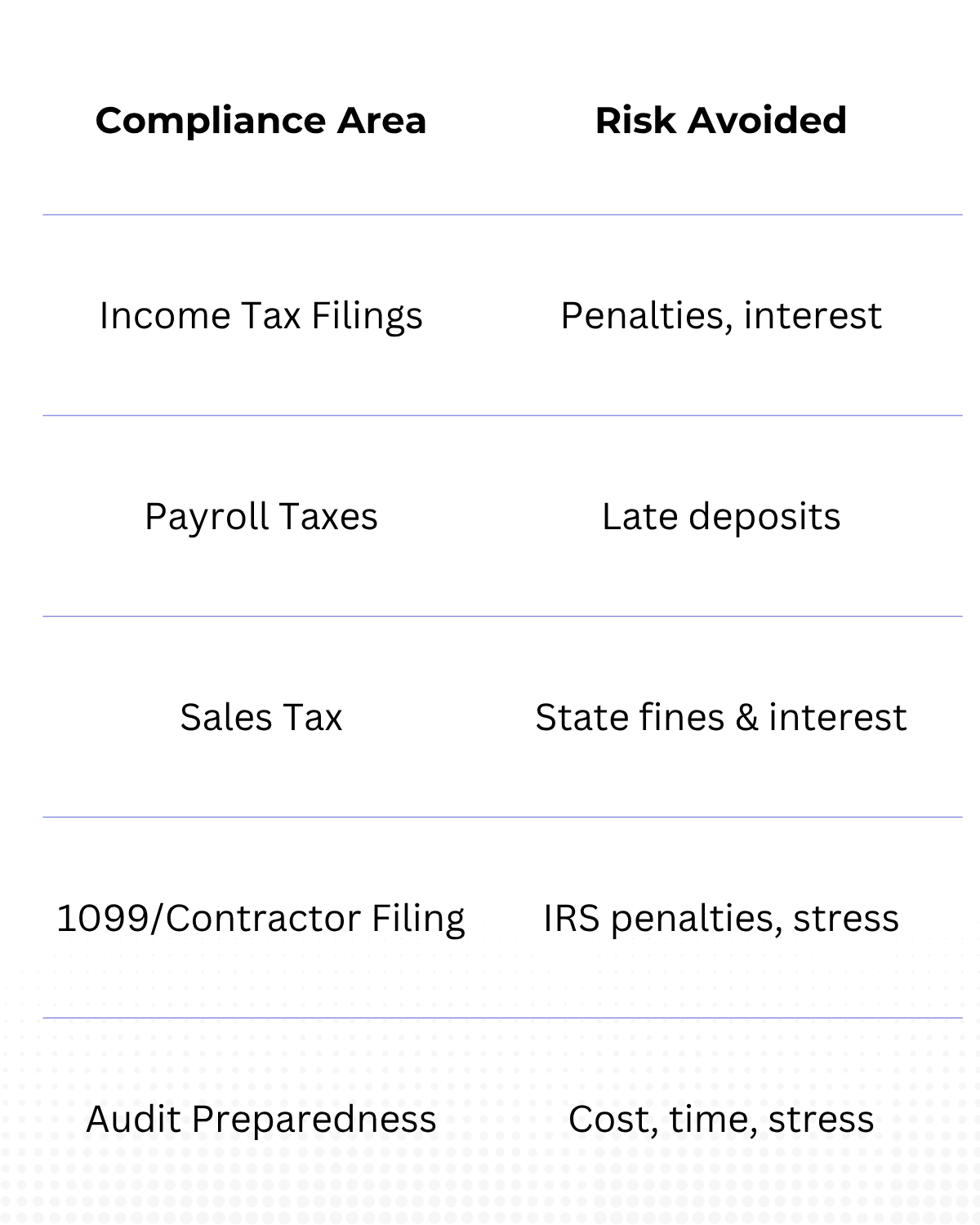

Why Year-Round Bookkeeping Prevents Risk

Clean Books = Fewer Problems

Regular bookkeeping isn’t optional, it’s your first line of defense against tax issues.

At FinStackk, we provide:

- Bookkeeping cleanup services

- Ongoing support for startups & small businesses

- Tools to stay ahead of audits and IRS scrutiny

Need help cleaning up your books or preparing for tax season?

Contact FinStackk today.